SINGAPORE (Jan 10): Why take risks? We get many questions about why, given the government-legislated CPF Ordinary Account interest rate of 2.5%, anyone should take a risk by investing their CPF money in the financial markets.

A Singapore government-guaranteed interest rate of 2.5% for your OA seems like a good idea, but we need to put that number into context, peel back the onion and think deeper about how markets and the economy work. However, before doing anything, we need to answer why we bother taking a risk at all, and how to be rewarded with returns for risks taken.

We hope to leave you with a framework to make better investment and financial planning decisions, especially with your CPF monies.

How does the government determine the CPF OA rate?

As stated by the CPF Board, “OA monies earn either the legislated minimum interest of 2.5% per annum, or the three-month average of major local banks’ interest rates, whichever is higher. The OA interest rate will be maintained at 2.5% per annum from Oct 1, 2019 to Dec 31, 2019, as the computed rate of 0.64% for bank rates is lower than the legislated minimum interest rate”.

We can say that the government is doing the people of Singapore a favour by paying 1.86% more than the three-month average interest rate of the major local banks for retirement savings. When bank interest rates were higher, the OA rate was higher, reaching 4.69% as recently as 1991. Since the year 2000, as interest rates have come down, the OA rate has stayed at the minimum legislated 2.50% (See Chart 1).

CPF OA rates compared with stock and bond market returns

We compared the CPF OA rates with the SGD returns of the MSCI All Country World Index (large-cap developed markets and emerging markets), MSCI World (large-cap developed markets only), Standard & Poor’s 500 (US large-caps) and Bloomberg Barclays Global Aggregate Bond Index (SGD-hedged) since 1990 (See Table 1).

Understanding the return characteristics of the different asset classes is important. One particularly important thing to consider is the success rate in beating the CPF OA interest rate by taking risks, and the amount of time you have to be invested to be reasonably certain of being successful (See Table 2). In general, as we increase the length of time invested, the success rate in performing better than leaving your money in the CPF OA increases. If you invested in diversified global stocks (such as the MSCI ACWI), you can expect that for almost 80% of 10-year rolling periods, you would have beaten the CPF OA interest rate by being invested. Over any 20year period, that number goes up to 100% certainty (looking at historical data).

It’s really about time. The longer the length of time, the better your success rate.

This makes a pretty compelling argument to take risks if you have a long enough investment horizon. That being said, you have to know yourself before doing so. Our behaviour and emotions often get in the way of capturing long-term market returns. Note the worst outcomes for shorter time periods in Table 3.

Can you live with a 40%+ loss on your investment value and still stay invested?

If not, then investing in 100% stocks is not a wise decision for any length of time, as those short-term shocks will knock you off course. Unfortunately, trying to time your way around these sharp drops is not possible to do with any degree of certainty, so we advise a lower-risk portfolio. If you invested in a globally diversified portfolio of 60% stocks and 40% bonds (60:40), that maximum loss decreases to 28%, but again, you need to be comfortable with riding out those shocks and taking this risk.

Generally, why do stocks compensate more than bonds, which compensate more than the CPF OA rate?

It is not random — it is structural. Stocks are legally and structurally riskier than bonds. If a company goes bankrupt, the bondholders will be paid before the company stockholders get anything. As a result, the market must generally compensate stockholders more for taking a greater risk than the bondholders. And the market must generally compensate the bondholders more than risk-free products. In the finance business, we call this the equity and credit risk premiums.

It’s all relative.

We may think of the CPF OA rate as something just set by the government, but it is not static. It moves with the market, inflation and the return on assets. It is highly unlikely that the government will be able to afford to pay an interest rate on CPF OA savings that is higher than riskier capital market returns for a sustained period of time. The money has to come from somewhere. Deflation (the ongoing decrease of the prices of goods and services) and hyperinflation (the rapid and out-of-control increase of the prices of goods and services; think Zimbabwe) aside, the relationship between risk and return should persist, and therefore returns of diversified stocks over bonds over the CPF OA rate should remain. Avoiding deflation and hyperinflation is in the interest of Singapore and its economic growth and relevance in the world. Monetary and fiscal policies are designed to avoid these scenarios.

What do all these numbers translate into in terms of $$$?

Let’s say you invested $50,000 in the MSCI ACWI. If you invested in January 1990, by September 2019, a period of almost 30 years, you would have $245,796, a 392% total return. Keeping your money in your CPF OA would give you $115,176, a 130% total return (See Chart 2).

Best-case scenario

In the best 20-year period, during which the 2008 global financial crisis occurred, you would have $188,840, a 278% total return. Keeping your money in your CPF OA would give you $85,931, a 72% total return (See Chart 3).

Worst-case scenario

In the worst 20-year period (you bought near the high of the dotcom boom in 1999 and sold at the depth of the flash crash at end-2018), you would have $96,989, a 94% total return. Keeping your money in your CPF OA would give you $82,394, a 65% total return (See Chart 4).

If you are unlucky, and do happen to catch the worst 20-year period, dollar-cost averaging — often referred to as a regular savings plan (RSP) — can give you a slightly better certainty of what your outcome will be. In the case of a $1,000 monthly investment subsequent to the $50,000 initial investment, you would have ended up with $488,091 versus $390,816 if left in your CPF OA (on a total principal investment amount of $289,000) (See Chart 5).

It is obvious from this study that two things matter: Time in the market (how long your money is in the market) and market timing. Unfortunately, timing the market is not possible to do consistently enough to beat the market with any certainty over the long term, and usually results in missing out on returns.

How do we give ourselves a higher confidence in capturing returns?

• Diversify globally. Recent history and the numbers represented in this study point to the S&P 500 as a generally superior way to have your money invested. While we do love the S&P 500 and it does make up a significant portion of the Endowus equities portfolios, it too can have extended periods of underperformance, such as a –9% total return in the entire decade of 2000 to 2009, during which emerging markets were up 162%. We do not know what the future will bring and urge our clients to diversify globally, across all developed and emerging markets.

• Be strategic, not tactical. Strategic asset allocation means investing and rebalancing towards an asset allocation that fulfils your needs, ambitions and future liabilities, with a behavioural risk tolerance suitable for you. Tactical asset allocation is trying to beat the market by timing your entry and exit, and changing your asset allocation based on the way you or an “expert” sees the world. Unfortunately, tactical rarely works, with an average investor return of 1.9% over the last 20 years (JP Morgan Asset Management’s Guide to the Markets, September 2019), likely due to fees and active trading.

• Manage your costs. A 1% difference in fees per year results in a 245% difference in returns after 30 years (assuming an annualised return after fees of 8% versus 7%).

• Fight for fair fees. Make sure that your adviser or banker is not being paid trailer fees, sales fees or other hidden commissions. This would incentivise them to churn your portfolio based on what is “hot” and pays higher commissions rather than a strategic allocation based on your goals and risk tolerance.

Thinking about the future: the Monte Carlo simulation

Based on the returns and volatility of returns of the CPF OA, MSCI ACWI and a 60:40 stocks and bonds portfolio since 1990, we ran Monte Carlo simulations 20 years into the future. You can see the concentration of red and grey lines in the $300,000-to-$500,000 range and a few outliers far above and a few below the CPF OA black line (ee Chart 6).

Do we know what will happen to markets tomorrow, next month or next year? Anyone who claims to know is likely very overconfident. We live in a world where even Jamie Dimon, the billionaire CEO of JP Morgan, one of the world’s biggest lenders, cannot call the direction of interest rates in the near term.

The markets will do what they do. But before you do anything, you have to ask yourself one important question: Do I think the world, with its population growth and technological innovation, will produce more goods and services 20 years from now?

If your answer is no, you should definitely keep your money in CPF while you have to, take it out of CPF as soon as your age allows, then spend all your money on a lifetime supply of canned food and bottled water. If your answer is yes, you should be invested. Find a way to participate in global markets. More goods and services = higher wages, more spending, growing companies, increasing asset prices, innovation and better efficiency in products and services, and an expanded stock market over the long term.

Be patient. Be humble. Be invested.

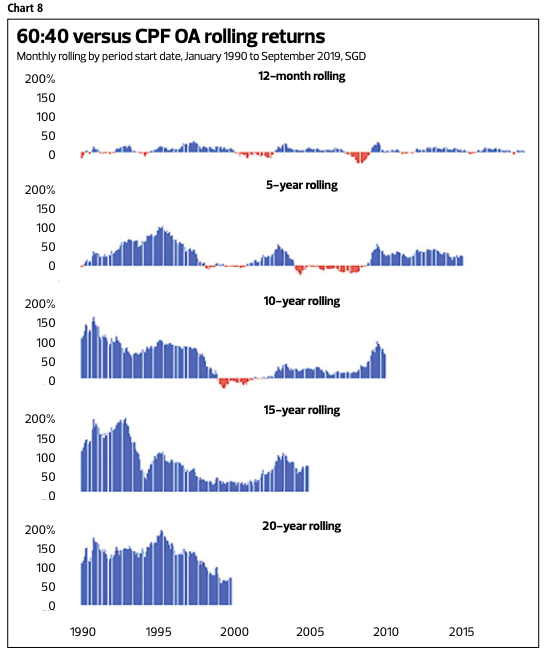

Two more charts

Charts 7 and 8 show the cumulative returns of the MSCI ACWI and 60:40 over the CPF OA for every starting month since January 1990. As you can see, as you move from 12 months rolling to longer time periods, the red decreases and the blue grows.

Gregory Van is co-CEO and chief operating officer of financial advisory firm Endowus