(July 15): On July 2, the Monetary Authority of Singapore published a consultation paper to consider raising the regulatory gearing limit (debt-to-asset ratio) for real estate investment trusts from the current 45%, and to introduce a minimum interest coverage ratio (ICR).

MAS says it is considering the option of allowing an S-REIT’s leverage to exceed 45% but not more than 50% if the REIT has a minimum ICR of 2½ times after taking into account the interest payments arising from the new debt (ICR threshold). “The leverage limit is not considered to be breached if the REIT’s ICR subsequently falls below the ICR threshold due to circumstances beyond the control of the REIT manager. However, the REIT should not incur additional borrowings or enter into further deferred payment -arrangements,” MAS says.

According to the consultation paper, MAS would also like to seek views on whether S-REITs with a higher ICR threshold should be allowed a higher leverage, say 55%.

The REIT Association of Singapore -(REITAS) has been canvassing and giving feedback to MAS for a couple of years now to raise aggregate leverage. Most S-REIT managers, analysts and REITAS office bearers view the move by MAS as a positive development. “The regulator will have a consultation to increase the regulatory limit of 45%, which is very low, considering [the REITs] are competing with the private funds out there, which have no regulatory limit,” says Jerry Koh, secretary of -REITAS and deputy managing partner at Allen & Gledhill.

Another rationale for raising aggregate leverage is that other developed markets do not have a regulatory limit, says Jonathan Quek, a member of the REITAS executive committee as well as managing director, head of Asia-Pacific real estate and lodging and head of Singapore investment banking at Citigroup Global Markets Singapore. “All developed markets have no leverage limit. Japan, Australia and the US have no regulatory limits. We are the only market out there that has such limits because the view here is that the market will [self] regulate,” he says.

However, MAS points out that Hong Kong imposes a leverage limit of 45% while Malaysia imposes a 50% limit. Thailand allows REITs to leverage up to 60% if they have an investment-grade credit rating. Belgium, Germany and the Netherlands have limits ranging from 60% to 66.25%.

S-REITs were allowed higher leverage limits until 2015. Rated S-REITs were allowed aggregate leverage of as high as 60%, while unrated REITs were limited to 35%. These limits were removed in 2015 to a single-tier of 45% after a consultation paper in 2014.

“Just because you are rated doesn’t mean you are a higher-quality REIT,” says Andrew Lim, president of REITAS and chief financial officer of CapitaLand. “Over the years, we think 45% is not commercial because REITs have to compete with other sources of capital [for assets] that have no issue with gearing.”

Because most S-REITs are inherently conservative, the industry practice has been to maintain an aggregate leverage of below 40% to respond to changing market conditions, such as declining property prices, notes UOB Kay Hian.

A higher gearing limit would allow some REITs such as retail REITs to acquire properties with greater ease, according to UOB Kay Hian. “For example, Frasers Centrepoint Trust was limited to acquiring just 30% of Waterway Point from its sponsor and would have considered acquiring the remaining 70% stake at a later stage. Having a higher leverage limit could pave the way for smaller S-REITs to acquire larger assets in one transaction,” UOB Kay Hian says.

All REITs’ ICRs are below proposed regulatory minimum

Interestingly, the ICRs of the 41 S-REITs are below the 2½ times (see Table 1) suggested by MAS. There are a couple of REITs whose ICRs are below three times, such as Far East Hospitality Trust at 2.93 times. -However, FEHT carries a relatively lower risk than REITs with overseas assets, as it has all its assets in Singapore, and all its borrowings are in local currency. Its sponsor is a unit of Far East Organization, one of the largest property groups in Asia. Elsewhere, Suntec REIT’s ICR is 2.9 times. Suntec REIT is one of the largest S-REITs.

Not all REITs disclose their ICRs. It is an easy enough computation, and MAS recommends using earnings before interest, taxes, depreciation and amortisation, or Ebitda, divided by interest expense. In general, non-cash items such as revaluation gains and mark-to-market foreign currency gains or losses are not included.

“To promote market transparency, MAS proposes to require REITs to disclose both their leverage ratios and ICRs in interim result announcements and annual reports. MAS notes that this is already the practice for some REITs,” the MAS announcement says. In general, 70% to 75% of -S-REITs disclose their ICRs. In particular, REITs with sponsors such as CapitaLand, Mapletree Investments, Frasers Property and Keppel Corp disclose their ICRs regularly. REITs that do not disclose ICRs are Far East Hospitality Trust, EC-World REIT, Lippo Malls Indonesia Retail Trust (LMIRT) and First REIT.

REITs with the highest ICRs are ParkwayLife REIT and Keppel DC REIT. ParkwayLife REIT’s Japanese nursing homes, financed by low-cost Japanese debt, have translated into an average cost of debt of just 0.91% and hence a high ICR of 13 times.

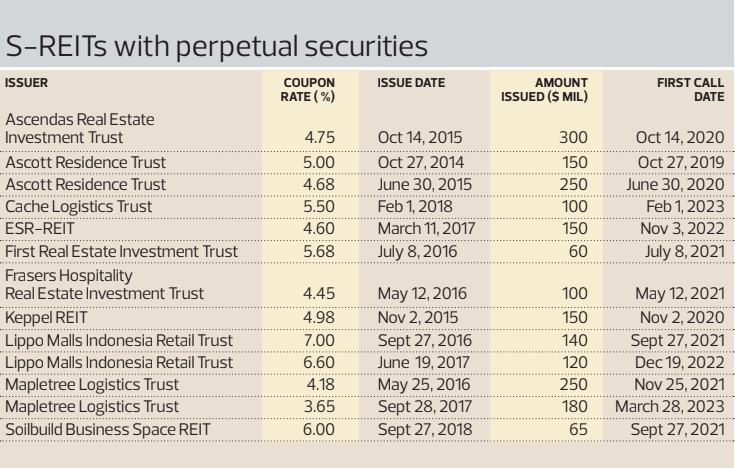

Classifying perpetual securities

Some 10 S-REITs have issued perpetual securities over the years (see Table 2). The first call date of Ascott Residence Trust’s $150 million of perpetual securities is in October this year. There is usually a step-up in interest expense if the securities are not called. Since risk-free rates have fallen this year, REITs looking to refinance perpetual securities are likely to use either plain vanilla notes or bank debt.

In the past two years, perpetual securities have been getting a bad rap, following Hyflux’s default of $900 million of retail perpetual securities and preference shares. The so-called retail PnPs were used as the equity portion to finance the Tuaspring Integrated Water and Power Plant.

Analysts have pointed out that perpetual securities understate a REIT’s actual leverage and this can be dangerous. “It’s timely to review the usage of perpetual securities by REITs along with the proposed changes in leverage limit,” says Vijay Natarajan, an analyst at RHB Securities.

Perpetual securities are classified as a form of equity. Hence, distributions on perpetual securities are not defined as interest expense and do not show up in -REITs’ ICRs. Instead, these distributions are grouped together with distributions to unitholders in the cash flow statement, or with dividends in the cash flow statement.

When asked about its view on perpetual securities, a MAS spokeswoman says: “We will consider all feedback from the public consultation on the minimum ICR threshold, including any suggestions and arguments on whether to include distributions on perpetual securities in the computation of the ICR.”

Some REITs include perpetual securities in their cost of debt. For instance, -LMIRT announces its all-in cost of debt excluding perpetual securities (5.12%) as well as its all-in cost of debt including perpetual securities (5.59%) in its quarterly statements. However, it does not announce its ICR either excluding or including perpetual securities.

REIT managers may consider giving unitholders the last say, according to RHB’s Natarajan. “One way to tackle raising the leverage limit is to [give unitholders the power to decide]. REITs can obtain a mandate [to raise the leverage limit] in an extraordinary general meeting like the share buyback and general mandates. That will allow unitholders to determine whether REIT managers are being sufficiently prudent when they raise leverage limits.”