SINGAPORE (Jan 31): In a recent interview, Dennis Khoo, regional head of TMRW digital group at United Overseas Bank (UOB), compared banks — including digital banks — to a car. What you see are the steering wheel, car seats, wheels, rims. But the engine is hidden.

“Lift the bonnet, and when you look at the car engine, you will see all the parts are connected. Banking is a bit like that. When you open the hood, you understand the complexity, how vital it is and why governments regulate it,” says Khoo. In Khoo’s view, digital banking and digital bank are different although three letters separate them.

Interestingly, consultants including PwC and Deloitte use the terms interchangeably. Digital banking is part of traditional banking, and another channel in an omnichannel strategy, says Khoo. Customers can perform their banking services anywhere – including from a laptop, mobile phone, ATM or banking branch. Digital banking is not a strategy on its own.

“It’s part of a bigger traditional bank set up where you have multiple channels. Every single channel that’s ever been invented is still around because you have to serve everyone especially if you are a major bank,” Khoo says. “A digital bank serves the customers of tomorrow today. Digital banking’s focus is to serve the customers of today well.” Digital bank is digital-only with no physical branches.

Marcus Liu, an analyst at CLSA, describes digital banks as those that can operate without any physical branch or ATM network. “They offer all of their facilities online and through mobile apps. Processes are typically automated so operational costs are lower. Accounts can be set up in minutes and money can be deposited through fund transfers. Users are typically of the younger, tech-savvy variety,” says Liu.

Bank of tomorrow

TMRW is UOB’s digital-only bank with no branches. Its model is to use data to engage customers as its primary goal and business model. Phrases like net promoter score (NPS) will be — in future — as common as cross-selling was in the past.

TMRW’s model is based on ATGIE — acquire customers who Transact to Generate data — from which TMRW gains Insights for further Engagement.

“Because costs for delivery of financial services are lower, digital banks can offer lower rates and lower fees to consumers. They can also potentially cater to underserved segments, although this is not TMRW’s strategy. [Digital banks] will [have to] compete on nimbleness and flexibility, which they will hope will offset their asset base disadvantage,” Liu of CLSA says.

Transaction services such as payments, CASA (current account savings account), credit cards and unsecured lending are services that do not require branches and can easily be done by digital-only banks. “Transactional banking is moving towards no branches in five to 10 years because regulation allows for non-face-to-face authentication,” Khoo says.

UOB has a dual strategy of operating a digital bank for millennials and to continue with digital banking for everybody. The 85-year-old bank serves its current customers which include mass-affluent and affluent customers through its UOB Mighty banking app as well as various other channels including its relationship managers. The plan is to acquire customers of tomorrow through TMRW, a digital-only bank with no physical branches.

Building a regional digital bank

UOB’s stated goal is to build TMRW into a regional digital bank in five Asean countries where it has subsidiaries or full bank licences. It is looking to garner three to five million customers in these Asean countries, while operating on a low cost-to-income ratio (CIR) of below 35%.

After launching in Thailand last year, TMRW is likely to be launched in either Indonesia or Vietnam next. Both countries have large pools of digitally-savvy millennials. TMRW has already had more than a million downloads.

In 2017, to kickstart implementing TMRW, UOB engaged and interviewed 500 young families in Bangkok. During this process, UOB learnt that its customers went through a lot of pain to remove fees. Concerns among the interviewees included poor service, and their propensity to overspend. In the feedback session, a millennial griped that the bank charges fees for CASA. “You are keeping my money and charging me for keeping my money,” the millennial said.

Although millennials are likely to be future high-value customers — given they are well educated and upwardly mobile —they are underserved and treated like mass-market customers. “We decided to choose a segment that has high future potential. Currently, the millennials may not have many assets and they may not earn a lot but their earnings will grow exponentially quickly because they are highly educated and highly mobile,” Khoo says.

TMRW encourages its customers to transact — it had a savings competition to engage users — and to generate data. It then uses insights from the data to get customers to become more active. Khoo brushes aside questions on the number of customers TMRW has and says he is tracking the number of active users – or customers who transact four times a month – and this is within expectations. “A lot of digital banks have admitted that engagement quality is poor because they haven’t focused on engagement,” Khoo points out.

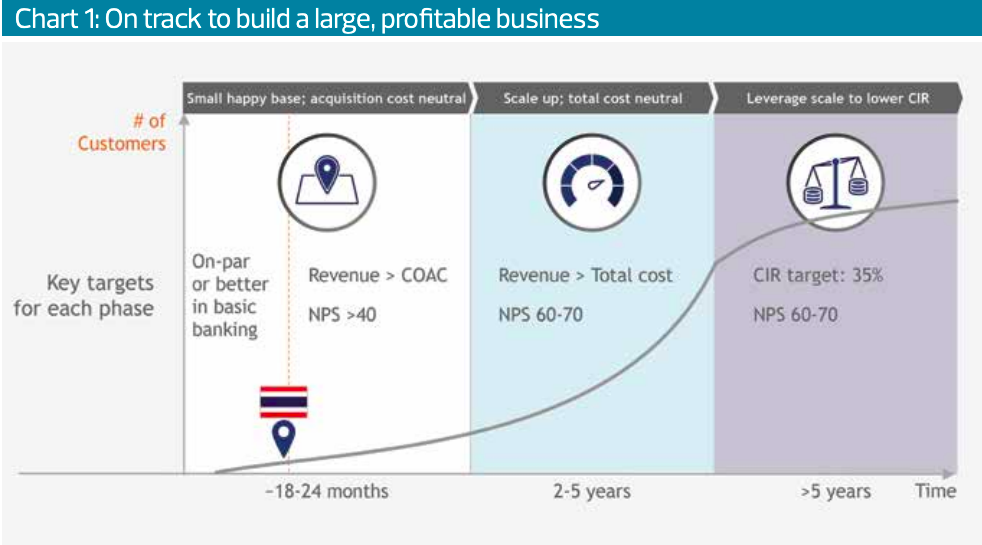

The strategy for TMRW requires a long-term commitment because there is a revenue mismatch. The potential revenue pool is worth at least $10 billion and TMRW has segmented the revenue potential in three phases (see chart 1).

In the first two years, the aim is to get a small base of happy customers who are willing to be your advocates by aiming for a NPS of more than 40. In Year 2 to 5, millennials are likely to have basic banking needs with small AUMs and credit amounts. Beyond Year 5, millennials will have more complex needs and this is when revenues should rise.

“Your costs are now but your money is going to come in future years. Revenue opportunity is small in the beginning with 1/10th of revenue apparent in year one to five,” Khoo cautions. “If you’re not an incumbent player, you won’t have the means. But if you don’t choose this group, you will be undifferentiated. We chose this group and we have the staying power.”

High NPS more important

Rather than focus on revenue early on, Khoo prefers to concentrate on NPS. This is an index that measures the willingness of customers to recommend a company's products or services to others. So, the higher the NPS score, the better. TMRW’s target is for its revenue to be higher than the cost of active customers, and to have a NPS of more than 40. For instance, if 50% of your customers like your product and are your promoters and 10% are detractors, NPS is 40.

“We are on track [for] 40. We’ve only operated for 10 months. We plan to exit two years [of operations] with NPS exceeding 40. When you have a high NPS, you have a lot of advocates, and then your cost of acquiring customers drops,” Khoo explains. Also, with high NPS, customers are less likely to switch main banks. “We need active, engaged customers who are advocates, which are your sales force at no cost,” Khoo reasons. “We plan to exit the first 24 months with revenue higher than the cost to acquire customers,” Khoo says (see chart 1).

Since UOB spent $100 million developing TMRW, it needs to make $20 from 5 million customers to cover costs. “I can recover that cost in two to five years. Once we’ve recovered total cost, we can drive CIR to a level lower than 35%,” Khoo says.

At that point, revenue exceeds the cost of acquiring customers and TMRW should reach its marginal breakeven. “After that, every single customer that comes in begins to pay back the unpaid capitalisation of your building [the infrastructure],” Khoo adds.

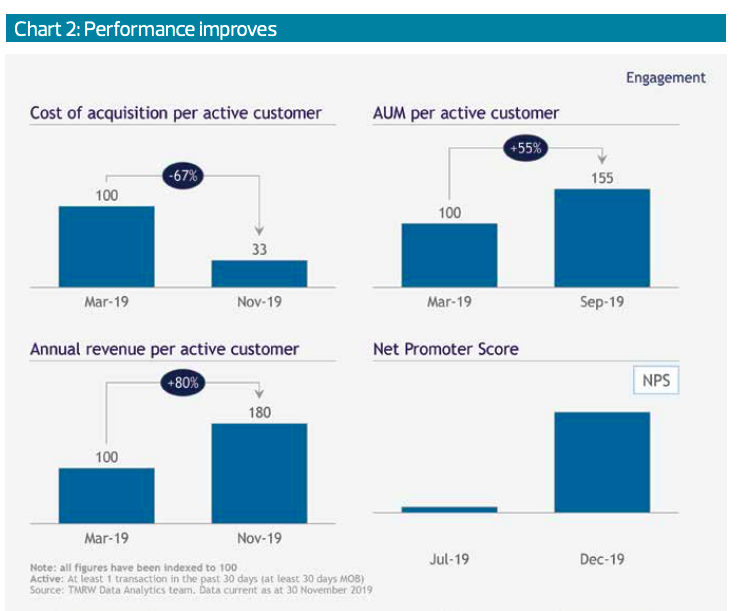

Already, the cost of acquisition per active customer has fallen by 67% in eight months, AUM per customer is up 55% while annual revenue per customer is up 80% (see chart 2).

Differentiating digital banks from digital banking

Khoo believes there are six factors that differentiate TMRW from other digital banking services and would give UOB a headstart compared to other Asean digital banks.

First, TMRW has an affinity among millennials; Secondly, TMRW’s user interface is uniquely simple and menu-less; Third, data is used to create insights to engage users; Fourth, the chatbot is designed around the customer so if the customer has a problem, TMRW will call the customer. For the fifth and sixth factors, Khoo says “we have a competitive bundle and we’ve put together the best of breed technology. To intertwine these six factors is not easy".

Liu of CLSA says UOB is likely to be the least affected by the new digital banks. “At this early stage, UOB stands to be least affected: At-risk fee pools are relatively lower; deposit base is not as large as that of DBS; cost of funds hasn’t got as much to potentially rise as DBS; and it is also nicely positioned on its digital journey.”

Meanwhile, being a mass-market retail-focused bank, DBS Group Holdings could be pressured if the new entrants compete on price, although it is the most advanced on its digital journey and could defend its position with digital offerings of its own. “OCBC is the least-well positioned digitally,” Liu says, adding that costs could rise with spending on technology.

“For TMRW, we want to create a good experience and remove as much friction as possible. We have always taken the positioning that there is digital bank and there is digital banking. When attackers come into Singapore, the defenders are doing digital banking while the attackers are doing digital banks. Some banks say you don’t need both. Although the jury is still out, we want to invest in both,” Khoo says.