WeWork’s IPO debacle emphasises that having a high-profile founder with a great idea is not enough

SINGAPORE (Dec 27): It was the most highly anticipated public offering of 2019. But that goal imploded spectacularly, almost bankrupting the company in the process.

WeWork — the US’ largest co-working provider — made headlines with its stalled IPO. But the fall of the latest industry darling — once labelled the “next Alibaba” — is causing investor nervousness, with some even calling for caution before buying into the next big thing.

But it is not the first tech start-up to buckle under the scrutiny of its finances and leadership from investors and the media. Medical company Theranos had raised millions of dollars and received federal approval before a damning Wall Street Journal investigation questioned its methods. The company faced a string of legal challenges as a result and shut down by September 2018.

WeWork did nothing illegal, but it was guilty of making big promises that resulted in middling profits.

Founded nine years ago, WeWork was valued at US$47 billion ($63.9 billion) before its botched IPO in October. This valuation would eventually drop to as low as US$10 billion, but the IPO was eventually axed after investors took a peek at documents that the company had filed in August with the US Securities and Exchange Commission and raised a stink over WeWork’s mounting losses, profitability model and unusual corporate governance structure.

For example, the company made losses of about US$900 million in 1HFY2019. The filing also unveiled other bizarre details — such as WeWork co-founder and CEO Adam Neumann’s erratic behaviour, which included smoking marijuana on private jets and promoting alcohol-fuelled company parties.

WeWork’s key backer SoftBank Group would eventually put up a US$9.5 billion rescue package in October. But that bailout was not without casualties: Neumann resigned on Sept 24 while thousands of workers were laid off.

This has also affected SoftBank’s earnings and, in a call with analysts, the Japanese conglomerate’s founder and CEO Masayoshi Son gave no indication of how WeWork would turn things around — perhaps astonishing for a portfolio company that has seen its investor’s US$6 billion investment reduced to US$1.3 billion as at Sept 30.

More scrutiny

It is also still unclear whether the ongoing struggles WeWork is facing in the US would have any impact on its operations in Singapore. But one thing is for certain, this fiasco shows that great ideas alone are not enough to build a business. Also, start-ups must now expect more scrutiny as they move forward.

Separate reports from venture capital (VC) fund Centro Ventures and financial data company Preqin have contrasting results of the number of deals done in Southeast Asia this year. For example, Centro’s report indicates a rise in the number of deals whereas Preqin says the opposite. Both reports show, however, that the amount of money doled out to start-ups by VCs fell in 2019 and, consequently, the total amount of money pumped into the ecosystem shrank.

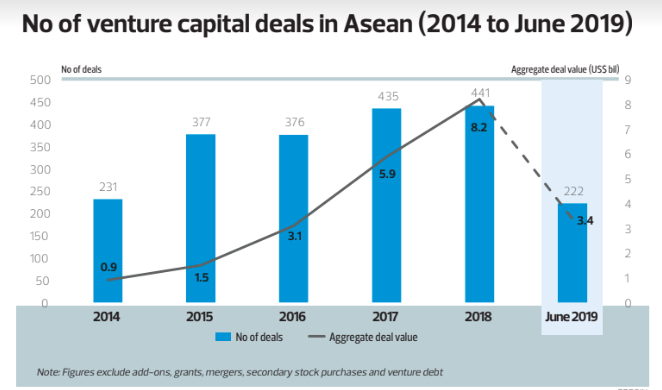

According to both reports, more than 200 deals were closed by end-June, with an aggregate deal value of US$3.4 billion. The Preqin report also noted growth in Series B and C financing, from US$600 million to US$1 billion in the period, suggesting that the so-called “valley of death” — the period in which a start-up has begun operations but has not generated revenue — financing gap for start-ups is narrowing.

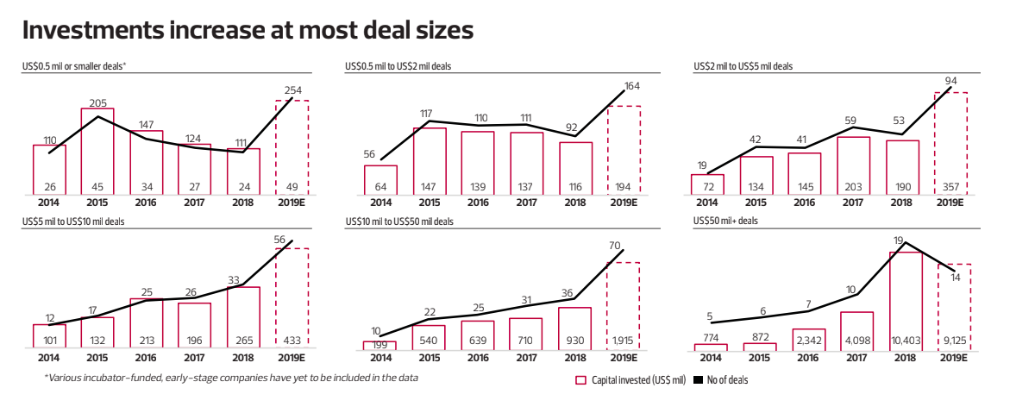

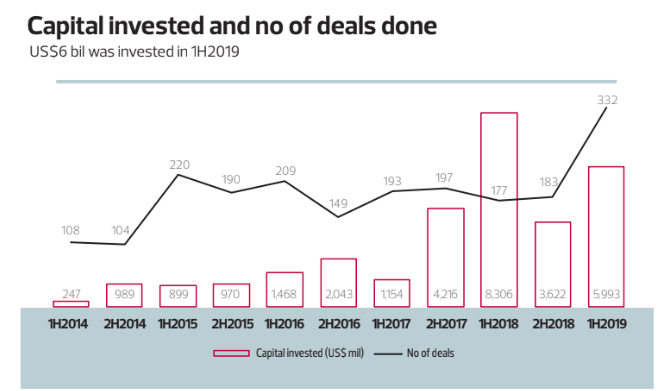

In Centro’s report, the aggregate deal value in Southeast Asia was higher than Preqin’s at US$6 billion, but deals included initial coin offerings, project financing and corporate spin-offs, and amounted to 332 transactions. The report also noted a rise in almost all deals, except for those worth US$50 million and above, which fell in 2019 to 14 from 19 the previous year.

Industry insiders tell The Edge Singapore that VCs and start-ups still see active funding despite cautiousness overseas.

Vihang Patel, co-founder of financial services start-up Finaxar, says: “[The funding] provides substantial dry powder for growing venture-backed companies. At the same time, there is a healthy deal flow at an early stage [pre-seed until Series A — a start-up’s first significant round of funding], owing to the growing number of new businesses set up.” Jupe Tsui, chief financial officer at Singapore-based hotel start-up RedDoorz, notes: “The fundraising landscape in Southeast Asia is still very active, even amid recent global events. While more mature markets such as the US may take a more cautious approach to viewing potentially inflated valuations of companies, it has not stopped VCs from investing in start-ups from this region, which is mainly due to the deal-making boom in Southeast Asia.” The more optimistic believe more deals are flowing through the region. Justin Hall, a partner at Singapore-based venture capital firm Golden Gate Ventures, says: “The fundraising landscape [in this region] is still very well capitalised. There are just as many deals and as much money flowing now as there were at least two years ago.” Damian Tan, managing editor of Vickers Venture Partners, concurs: “We are seeing better targeted companies aiming to solve global problems led by expert founders.

Founders are also getting better at building good companies. Money into start-ups is also increasing year-on-year, as the VC and start-up ecosystem grows overall globally.” Still, investors are now more discerning.

“The fundraising landscape is slightly trickier, but money and deals are still free flowing. Investors have become more focused on quality and less on [the growth of the customer base or markets],” says RHL Ventures managing partner Rachel Lau.

Chinese investment is also rising in this arena, according to RedDoorz’s Tsui, who sees the region’s unicorns — start-ups valued at $1 billion and above — successful in raising sizeable funding rounds.

“Southeast Asia’s start-ups saw Chinese VC investments grow more than eight times year-on-year to US$1.78 billion in the first seven months of 2019 — a clear indicator that others are looking at the region more closely than ever before,” says Tsui.

Governance versus culture

WeWork’s IPO failure and Uber’s culture issues also highlight the importance of corporate governance. As RHL’s Lau says: “Corporate governance is the emphasis for investors as well, given how the bigger companies such as Uber and Airbnb have shown a terrible track record in protecting investor rights.”

Tsui agrees, noting that Southeast Asia’s “young and diverse” ecosystem means it is crucial that founders and investors apply basic policies and financial controls from an early stage to ensure operations are scrutinised and funds are well managed.

“The proof of good corporate governance will also enable start-ups to attract bigger investors at higher valuations,” he says. “It will always be a priority for RedDoorz, especially given the rate in which we’ve scaled the business across the region. We continue to hire the right people to manage our operations, business and funds, and we employ rigorous financial controls.”

Some VCs say corporate governance should not be confused with subsidies and discounts. “Scrutiny of all costs and expenditures is a hallmark of good corporate governance, and that has always been the case,” says Golden Gate’s Hall.

Sustainable business models are key, according to VCs, with more scrutiny on whether start-ups can show a clear path to profitability rather than growth at all costs.

“Recently, it has been shown that good and profitable transactional growth, or companies with a clear line to profitability and sustainable margins, are better than growth that appears unsustainable and growing just for eyeballs or customer acquisition,” says Vickers’ Tan.

“For many VCs, the quality of corporate governance has been important but, for very young companies, their priorities have been invention and selling; so, that’s perhaps acceptable. But, once [the companies start to take off], the governance must follow. For Vickers, we typically sit on the board and are critical of good governance. Best practices are there because they work.”

Investors are aware that discounts and subsidies are still strategies that start-ups will continue to pursue for customer acquisition, and there is an expectation that the businesses will be sustainable in the long run. As such, investors are once again focusing on the fundamentals of business to ensure start-ups give better returns.

Finaxar’s Patel says: “Good governance practices have always shown positive impact on the growth of the company traditionally. It was previously hard for entrepreneurs — many of whom were first-timers in Southeast Asia — to be able to exercise that level of diligence. Thus, it was also hard for VCs to expect such diligence. That has changed with the maturing of the ecosystem; entrepreneurs have much better support both internally [via experienced hires] and externally via various start-up programmes to imbibe these practices while running the company.”

There seem to be mixed views on how investors view start-ups now, with some industry insiders saying investors are turning cautious while others saying nothing has changed. Despite the cautiousness, investors are not adding downside protection clauses into term sheets.

“Investors are more cautious today than five years ago, but that’s also because the cheque sizes are bigger today,” says Tsui.

Vickers’ Tan says: “We are always adjusting and refining term sheets; in fact, we have tended to remove requirements rather than add them on. From our perspective, we are not more cautious of signing term sheets or adding terms.”

Golden Gate’s Hall says: “Investors in Southeast Asia have continued to sign term sheets at as fast a clip now as they have in the previous 12 months. I have not seen anything needlessly untoward in these term sheets, such as unfriendly downside protections.”

RHL’s Lau disagrees, noting that “previously, term sheets were given out without seriously considering the downside protection or putting in corporate governance clauses — buyback, [right of first refusal], board seats, monthly operating metrics.” The start-up scene has matured in

recent times and now operates on a more level playing field in terms of obtaining funding.

Says Patel: “As the number of start-ups grew, experienced VCs started entering the market, and we saw standardisation in basic terms for early-stage investments. For example, the use of SAFE (simple agree-ment for future equity) was hardly seen before 2016 but, since then, large numbers of pre-seed and seed rounds are done on this simple document.”

‘Less tolerant’

Moving ahead, VCs and start-ups can expect costs to be scrutinised. “We are less tolerant towards companies that are burning cash to sustain growth,” says RHL’s Lau.

Southeast Asia is also seeing more logistics and social commerce start-ups emerge as the next high-growth sectors. “I expect both verticals to become extremely well capitalised over the next few years,” says Golden Gate’s Hall.

Unicorns are also starting to proliferate in the region as Grab is joined by others such as Carousell, whose latest valuation is more than $1 billion. Vicker’s Tan says these start-ups are everywhere and not just in the US. “China has herds of them and Asia is rising as a good investible opportunity,” he says.

Tsui notes that Southeast Asia’s internet firms drew in US$7.6 billion in 1H2019, up 7% y-o-y, which is as a good sign, citing Temasek, Google and Bain report “e-Conomy SEA 2019”.

He adds: “This would indicate that the region is moving in the right direction.

None of this would have been possible if there wasn’t a robust and cohesive ecosystem. There are more companies now heading towards their Series C than before, and there are some solid VCs that are able to add value to these firms on their journey towards a logical conclusion.”

What are the trends to look out for next year? For Golden Gate’s Hall, the financial technology start-ups will be one to watch.

“The proliferation and rise of challenger banks will be a notable trend for 2020, as well as the continued emergence and consolidation of digital payments infrastructure across and within numerous verticals,” he says.

RHL’s Lau sees a potential storm ahead for start-ups. As such, they need to focus on fundamentals because, rather than those who are intent on growing at all cost, it is “companies that are able to withstand a potential cash crunch, and are innovative and really looking to disrupt existing ways of doing business” that will survive.

This view is echoed by Finaxar’s Patel, who sees a tempering of “irrational exuberance” in the ecosystem towards fundraising and valuation, leading to an overemphasis on top-line growth.

“It will be a good ‘reset’ in the coming years to allow investors and founders to focus on creating enduring companies with a mission to deliver products or services that have a positive impact on the world we live in, not which companies have the biggest war chest to outcompete others through negative blitz scaling,” he says.

“We also see an increase in large corporates directly working with start-ups closer than ever before. This could be via their venture arm or through direct strategic investment. A key part is that all these go beyond financing, and looking at the ways to increase reach for these start-ups, from revenue, product portfolio and geographical standpoint, which otherwise would not have been possible by the start-up on its own. These closer partnerships are now seeing tangible results, especially in the areas of financial services, logistics, real estate and e-commerce.”

Still, start-ups should also stick to the tried and tested, reckons Vickers’ Tan.

“Ideas are no longer just a whim but opportunities that are well thought out and tested, and the dedication and drive to succeed is even greater. There are lots of problems in this world to solve and more people are willing to invest in solving them. It’s becoming a viable option versus working for a big firm for the rest of your life. So, VCs have a lot to invest in.”

As start-ups work towards profitability, Tsui notes that VC investment is surging, and more unicorns are appearing on the horizon. “As a result, investors may also want to focus on predicting consumer trends earlier and funding at the seed stage to the Series B and C stages. Not only that, but VCs could also back their prized companies for longer periods of time; if these start-ups are able to prove their worth by monetising their services, they’d be on track to becoming unicorns,” he concludes.

“We believe next year will see some interesting milestones for companies in this region. While on that growth journey, firms at every stage will need to prioritise corporate governance, particularly in a highly fragmented region with a fractured regulatory environment.”