As the US and China conclude their ‘phase one’ discussions, is the end to the trade war really in sight?

SINGAPORE (Dec 27) : After almost two years of trade war and several hiccups in arriving at a truce, US Trade Representative Robert Lighthizer says ‘phase one’ of negotiations between the US and China is “totally done”. In a late night briefing on Dec 13, China’s vice-commerce minister, Wang Shouwen, confirmed that the US had agreed to cancel some of its existing tariffs on Chinese goods.

Under the deal, announced on Dec 13, the US will reduce some tariffs on Chinese goods, in exchange for a US$200 billion ($271 billion) increase in Chinese imports of US agricultural, manufactured and energy products over the next two years.

Lighthizer explained that the US will maintain the 25% tariffs imposed on US$250 billion of Chinese imports, while halving tariffs on US$120 billion of products from the current 15% to 7.5%. This reduction will take effect within 30 days of the signing of the deal, which is slated for the first week of January. The nitty gritty details of the agreement will be worked out by January.

Market watchers The Edge Singapore spoke to concur that the deal will give economies worldwide reprieve from the overhang of uncertainty and poor trade volumes. Says Mohamed Faiz Nagutha, ASEAN Economist at the Bank of America Merrill Lynch: “It was a little better than we had expected. We were looking at a deal and not further escalation of tariffs; we did not expect a rollback on tariffs that have already been imposed”.

Credit Suisse says in a Dec 16 titled China Market Strategy, that the deal is “a good beginning and an opportunity for both sides to build trust”. While it is unlikely to offer direct help to industrial investment and consumer confidence, particularly in China, it can “give the market some assurance and breathing room for a while,” it adds.

Deep wounds

Nagutha cautions that weakness in the global economy “is quite deep and will take some time to recover”. Prior to the deal, the International Monetary Fund (IMF) in October, forecast global economic growth of 3% for 2019 – the slowest pace since the financial crisis a decade ago.

To make matters worse, the tensions had, at their peak, advanced to a stage that “threaten[ed] to drive the US and other global economies into a recession,” notes Michael Spencer, Chief Economist and Head of Research for Asia-Pacific at Deutsche Bank.

Data from the US’ Commerce Department shows its GDP grew 1.9% y-on-y in 3Q2019. While this is better than the 1.6% forecast, it is below the 3.4% chalked up in 3Q2018 and is the slowest quarterly growth so far this year. China’s GDP growth of 6% in 3Q2019 missed the consensus forecast of 6.1% and is its slowest growth rate in 27 ½ years.

Singapore too has been a casualty of the trade war, given its export-oriented economy, in which the value of trade is more than three times the size of GDP. While the city state maintained a positive growth rate of 0.1% in 3Q2019, it marginally escaped a technical recession, defined as two consecutive quarters of negative growth. The other ASEAN countries have been feeling the pinch too, particularly from a cut back in exports by China owing to lower exports to the US (see Chart 1).

Despite the truce, the IMF estimates the trade war could reduce global GDP by 0.8% by 2020. This is due to the detrimental effects of the tariffs on the demand for manufacturing, automobiles, semi-conductors and capital goods. Tian Lin, an Assistant Professor at INSEAD who specialises in international trade and spatial economics, says hypothetically, a 25% tariff levied on all imports during the trade war, will significantly increase the total production cost of the products, in the global value chain.

Using the production of T-shirts as an example, Tian says, the three stage-process involves the US exporting raw cotton to India which then processes it into fabric and exports it to China for the material to be stitched and made ready for sale, most likely, to US consumers. “Now during a trade war, if each country involved in the value chain [is levied with a] 25% tariff, the tariff will be paid three times, each time it crosses the border,” Tian tells The Edge Singapore.

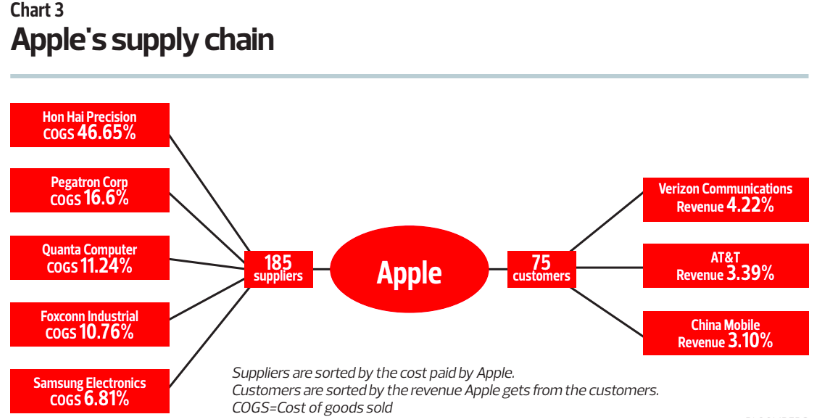

With textile exports from China having inputs from Japan, Korea and Asean (see chart 2), Tian’s example illustrates the spillover effect of the US’ tariffs on multiple countries. The T-shirt is one example of an item with inputs from several countries. In more extreme supply chains such as the production of Apple’s iPhones, MacBooks and iPads, over 180 products are sourced from some 25 countries. Apple itself has 75 customers (see Chart 3). This means a tariff imposed on an electronic gadget assembled in China, spills over to the 24 other countries, thereby affecting their trade balances as well.

Changing supply chains

To circumvent these price hikes, Chinese firms have adopted a “substitution effect”, says Vishnu Varathan, head of economics and strategy at Mizuho bank. This involves shifting their production facilities to cheaper countries in Southeast Asia, to evade the tariffs imposed on the Chinese-exported goods.

Vietnam for one, opened its doors to such firms. It took on a bigger role as an assembly destination for different raw materials –previously assumed by China. And while it benefitted from a 7.31% growth in 3Q2019 – one of the highest in the region – that was short-lived. US President Donald Trump soon imposed tariffs on Vietnam’s exports produced by Chinese firms, which cancelled the net benefits the country was originally reaping. Moreover, Deutsche Bank’s Spencer says the cost of production in Vietnam increased significantly because of the higher demand for services thereby making the cost savings of producing in that country negligible.

“The benefit of lower prices was lost to Chinese firms eventually as the US slapped it with tariffs,” notes Vishnu, adding that the US’ intention was to protect its domestic markets from any country. The World Trade Organization notes that products are being marked as “Made in The World” rather than in one country. It highlights that an imposition of tariffs may eventually backfire on the country that introduced them, as they could lead to increased costs. This is seen in the current trade war.

To avoid such costs, Tian notices firms “re-shaping their supply chains” through a consolidation of production into fewer countries. “A consolidation will minimise cross border dealings and the higher costs such as transportation and logistics, that come with it”, she notes. Tian believes such consolidation will incentivize firms to increase their pace of innovation to expedite the production and quality of the product.

ASEAN has already felt the effects of the changing supply chains, notes Bank of America’s Nagutha. He says the extent of the impact can be broken down into three tiers : investment hothouses, countries that received interest, and countries that did not reap as much benefit as they could have. The first tier comprises Vietnam, the sole country that saw higher investments. The second tier consists of countries such as Malaysia and Thailand which issued more approvals to US and Chinese manufacturers to shift their operation bases, although that did not translate into higher investments. In the last tier are countries such as Indonesia, which should have benefited because of its low labour cost and large population base, are parked in the last tier.

Looking ahead, Steen Jakobsen, Chief Investment Officer at Saxo Bank thinks the world will eventually split in two comprising the US and a new Washington consensus in one part, and China at the centre of the other. Global growth will operate in two separate platforms, he predicts, adding that this will translate into lower trade volumes and growth, less division of labour and a resultant decrease in economic growth and productivity.

Tariffs again in 2021?

With preparations for the phase one of the US-China trade deal are underway, Trump is already gearing up for ‘phase two’. He has tweeted that the US will begin negotiations on the second phase of the deal immediately, rather than waiting until after the 2020 US elections. However, Lighthizer cautions that a trade war truce would not solve all the problems between the US and China, because integrating China’s state-dominated economic system with America’s private-sector led system, will take years.

Both Jakobsen and Nagutha say the delay in scheduling the phase one talks is an indication of the difficulties faced in reaching common ground. Even so, the duo do not expect further tariffs till after the US elections, as Trump tries to protect consumers’ interests and shield employees in the affected industries. That is not to say that there will be a complete stop in the trade war with no further tariffs in 2021, observes Nagutha.

If the Democratic Party retains the House of Representatives and wins the Senate in 2020, it is just as likely to take a hard-line stance on China. One of the leading contenders for the Democratic nomination for president, Elizabeth Warren reportedly said Trump was too lenient on China in the phase-one agreement.

For now, the US seems to have found itself a new enemy: Europe. “The US has a very unbalanced relationship with Europe on trade, with an annual bilateral deficit of up to US$180 billion this year,” says Lighthizer. The main issue he says, is “a lot of barriers to trade and a lot of other problems [the US] has to address there”. The US imposed tariffs on US$7.5 billion of European Union goods in October, following a dispute over aircraft subsidies. It is now looking to levy taxes on a multiple products randing from Italian cheese, to French wines and British whisky.