All this just means that trying to predict stock market movements is a fool’s errand. Narratives, it seems, do not move stock prices. Rather, reasons are provided for stock movements, after the fact. As value investors, we would be much better off looking at the underlying business, earnings, cash flows and balance sheets instead of trying to time the market.

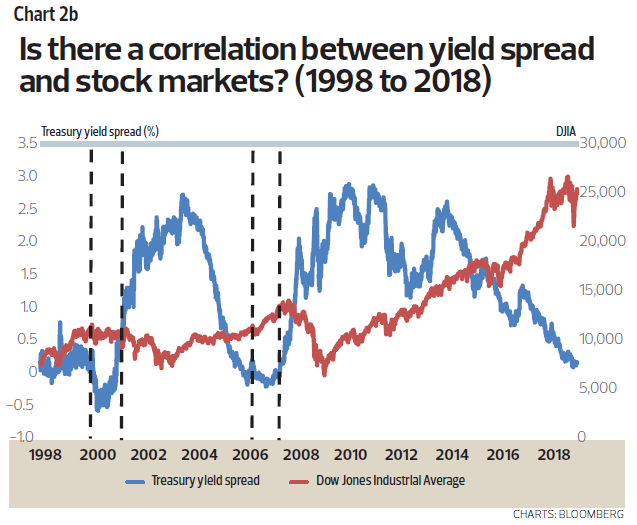

Is a recession imminent?

Economic cycles of expansions and recessions are as inevitable as death and taxes. But I do not think there is any fundamental reason for economic expansion to die from old age.

All this just means that trying to predict stock market movements is a fool’s errand. Narratives, it seems, do not move stock prices. Rather, reasons are provided for stock movements, after the fact. As value investors, we would be much better off looking at the underlying business, earnings, cash flows and balance sheets instead of trying to time the market.

Is a recession imminent?

Economic cycles of expansions and recessions are as inevitable as death and taxes. But I do not think there is any fundamental reason for economic expansion to die from old age.

Investor sentiment for equities stayed positive amid rising expectations of a US-China trade deal, while a more dovish Fed is aiding the recovery in emerging-market currencies.

Last week’s gains pared total portfolio losses to just 4.1% since inception. By comparison, the MSCI World Net Return Index is down a lesser 0.4% over the same period.

Tong Kooi Ong is chairman of The Edge Media Group, which owns The Edge Singapore

Investor sentiment for equities stayed positive amid rising expectations of a US-China trade deal, while a more dovish Fed is aiding the recovery in emerging-market currencies.

Last week’s gains pared total portfolio losses to just 4.1% since inception. By comparison, the MSCI World Net Return Index is down a lesser 0.4% over the same period.

Tong Kooi Ong is chairman of The Edge Media Group, which owns The Edge Singapore

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks, including the particular stocks mentioned herein. It does not take into account an individual investor’s particular financial situation, investment objectives, investment horizon, risk profile and/or risk preference. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.